Keynesian economics

From dKosopedia

Keynesian economics, or Keynesianism, is an economic theory based on the ideas of John Maynard Keynes, as put forward in his book The General Theory of Employment, Interest and Money, published in 1936 in response to the Great Depression of the 1930s.

In Keynes's theory, general (macro-level) trends can overwhelm the micro-level behavior of individuals. Instead of the economic process being based on continuous "supply side" improvements in potential output, as most classical economics had focused on from the late 1700s, Keynes asserted the importance of the aggregate demand for goods as the driving factor, especially in downturns. From this he argued that government policies could be used to promote demand at a "macro" level, to fight high unemployment of the sort seen during the 1930s.

A central conclusion of Keynesian economics is that there is no strong automatic tendency for output and employment to move toward full employment levels. This conflicts with the assumptions of supply side economics, Austrian economics and much of neoclassical economics, that price adjustment will achieve this goal. More broadly, Keynes saw his as a general theory, in which resource utilization could be high or low, whereas previous economics focused on the special case of full utilization.

Contents |

Historical background

John Maynard Keynes was one of a wave of thinkers who perceived increasing cracks in the assumptions and theories which held sway at that time. As physics questioned the necessity of absolute time, writers the structured narrative, and composers the need for tonal harmony -- Keynes questioned two of the pillars of economic theory dominant: the need for a solid basis for money, generally a gold standard, and the theory, expressed as Say's Law which stated that decreases in demand would only cause price declines, rather than affecting real output and employment. In his political views, Keynes was no revolutionary. He was pro-business and pro-entrepreneur, but was very critical of rentiers and speculators, from a somewhat Fabian perspective. He was a "new" or modern liberal.

It was his experience with the Treaty of Versailles which pushed him to make a break with previous theory. His "The Economic Consequences of the Peace" (1920) not only recounted the general economics, as he saw them, of the Treaty, but the individuals involved in making it. The book established him as an economist who had the practical political skills to influence policy. In the 1920s, Keynes published a series of books and articles which focused on the effects of state power and large economic trends, developing the idea of monetary policy as something separate from merely maintaining currency against a fixed peg. He increasingly believed that economic systems would not automatically right themselves to attain "the optimal level of production." This is expressed in his famous quote, "In the long run, we are all dead", implying that it doesn't matter that optimal production levels are attained in the long run, because it'd be a very long run indeed. However, he neither had proof, nor a formalism to express these ideas.

In the late 1920s, the world economic system began to break down, after the shaky recovery that followed World War I. With the global drop in production which eventually became "the Great Depression," critics of the gold standard, market self-correction, and production-driven paradigms of economics moved to the fore. Dozens of different schools contended for influence. Further, some pointed to the Soviet Union as a successful planned economy which had avoided the disasters of the capitalist world and argued for a move toward socialism. Others pointed to the alleged success of fascism in Mussolini's Italy.

Into this void stepped Keynes, promising not to institute revolution but to save capitalism. He circulated a simple thesis: there were more factories and transportation networks than could be used at the current ability of individuals to pay and that the problem was on the demand side.

But many economists still insisted that business confidence, not lack of demand, was the root of the problem, and that the correct course was to slash government expenditures and to cut wages to raise business confidence and willingness to hire unemployed workers. Yet others simply argued that "nature would take its course," solving the Depression automatically by "shaking out" unneeded productive capacity.

Keynes and the Classics

Keynes explained the level of output and employment in the economy as being determined by aggregate demand or effective demand. In a reversal of Say's Law, Keynes in essence argued that "demand creates its own supply," up to the limit set by full employment.

In "classical" economic theory -- Keynes's term for the economics prior to General Theory (and specifically that of Arthur Pigou) -- adjustments in prices would automatically make demand tend to the full employment level. Keynes, pointing to the sharp fall in employment and output in the early 1930s, argued that whatever the theory, this self-correcting process had not happened.

In the classical theory, the two main costs are those of labor and money. If there was more labor than demand for it, wages would fall until hiring began again. If there was too much saving, and not enough consumption, then interest rates would fall until either people cut saving or started borrowing. These two price adjustments would always enforce Say's Law, and therefore the economy would be at the optimal level of output.

Wages and spending

Even in the worst years of the Depression, the classical theory defined economic collapse as simply a lost incentive to produce. Mass unemployment was caused only by high and rigid real wages. The proper solution was to cut wages.

To Keynes, the determination of wages is more complicated. First, he argued that it is not real but nominal wages that are set in negotiations between employers and workers. It's not a barter relationship. First, nominal wage cuts would be difficult to put into effect because of laws and wage contracts. Even classical economists admitted that these exist; unlike Keynes, they advocated abolishing minimum wages, unions, and long-term contracts, increasing labor-market flexibility. However, to Keynes, people will resist nominal wage reductions, even without unions, until they see other wages falling and a general fall of prices.

He also argued that to boost employment, real wages had to go down: nominal wages would have to fall more than prices. However, doing so would reduce consumer demand, so that the aggregate demand for goods would drop. This would in turn reduce business sales revenues and expected profits. Investment in new plant and equipment -- perhaps already discouraged by previous excesses -- would then become more risky, less likely. Instead of raising business expectations, wages cuts could make matters much worse.

Further, if wages and prices were falling, people would start to expect them to fall. This could make the economy spiral downward as those who had money would simply wait as falling prices made it more valuable -- rather than spending. As Irving Fisher argued in 1933, in his Debt-Deflation Theory of Great Depressions, (falling prices) can make a depression deeper as falling prices and wages made pre-existing nominal debts more valuable in real terms.

Excessive saving

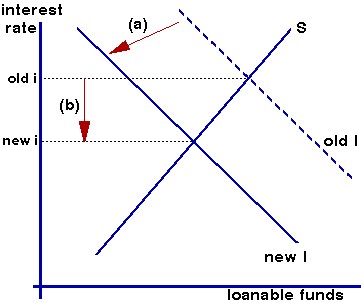

The classical economists argued that interest rates would fall due to the excess supply of "loanable funds." The first diagram, adapted from the only graph in The General Theory, shows this process. (For simplicity, other sources of the demand for or supply of funds are ignored here.) Assume that fixed investment in plant and equipment falls from "old I" to "new I" (step a). Second (step b), the resulting excess of saving causes interest-rate cuts, abolishing the excess supply: so again we have saving (S) equal to investment. The interest-rate fall prevents that of production and employment.

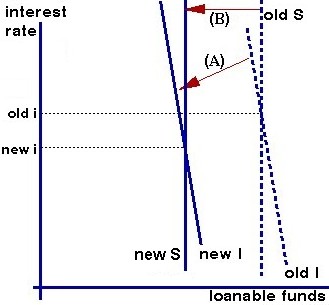

Keynes had a complex argument against this laissez faire response. The graph below summarizes his argument, assuming again that fixed investment falls (step A). First, saving does not fall much as interest rates fall, since the income and substitution effects of falling rates go in conflicting directions. Second, since planned fixed investment in plant and equipment is mostly based on long-term expectations of future profitability, that spending does not rise much as interest rates fall. So S and I are drawn as steep (inelastic) in the graph. Given the inelasticity of both demand and supply, a large interest-rate fall is needed to close the saving/investment gap. As drawn, this requires a negative interest rate at equilibrium, though this is not necessary to the argument.

Even if this "trap" does not exist, there is a fourth element to Keynes's critique. Saving involves not spending all of one's income. It thus means insufficient demand for business output, unless it is balanced by other sources of demand, such as fixed investment. Thus, excessive saving corresponds to an unwanted accumulation of inventories, or what classical economists called a "general glut". This pile-up of unsold goods and materials encourages businesses to decrease both production and employment. This in turn lowers people's incomes -- and saving, causing a leftward shift in the S line in the diagram (step B). For Keynes, the fall in income did most of the job ending excessive saving and allowing the loanable funds market to attain equilibrium. Instead of interest-rate adjustment solving the problem, a recession does so. Thus in the diagram, the interest-rate change is small.

Finally, a recession undermines the business incentive to engage in fixed investment. With falling incomes and demand for products, the desired demand for factories and equipment (not to mention housing) will fall. This accelerator effect would shift the I line to the left again, a change not shown in the diagram above. This recreates the problem of excessive saving and encourages the recession to continue.

In sum, to Keynes there is interaction between excess supplies in different markets, as unemployment in labor markets encourages excessive saving -- and vice-versa. Rather than prices adjusting to attain equilibrium, the main story is one of quantity adjustment allowing recessions and possible attainment of underemployment equilibrium.

Active fiscal policy

As noted, the classicals wanted to balance the government budget, through slashing expenditures or (more rarely) raising taxes. To Keynes, this would exacerbate the underlying problem: following either policy would raise saving (broadly defined) and thus lower the demand for both products and labor. For example, Keynesians see Herbert Hoover's June 1932 tax hike as making the Depression worse.

Keynes's ideas influenced Franklin Delano Roosevelt's view that insufficient buying-power caused the Depression. During his presidency, he adopted some aspects of Keynesian economics, especially after 1937, when, in the depths of the Depression, the United States suffered from recession yet again. Something similar to Keynesian expansionary policies had been applied earlier by both social-democratic Sweden and Nazi Germany. But to many the true success of Keynesian policy can be seen at the onset of World War II, which provided a kick to the world economy, removed uncertainty, and forced the rebuilding of destroyed capital. Keynesian ideas became almost official in social-democratic Europe after the war and in the U.S. in the 1960s.

Keynes's theory suggested that active government policy could be effective in managing the economy. Rather than seeing unbalanced government budgets as wrong, Keynes advocated what has been called counter-cyclical fiscal policies, that is policies which acted against the tide of the business cycle: deficit spending when a nation's economy suffers from recession or when recovery is long-delayed and unemployment is persistently high -- and the suppression of inflation in boom times by either increasing taxes or cutting back on government outlays. He argued that governments should solve short-term problems rather than waiting for market forces to do it, because "in the long run, we are all dead."

This contrasted with the classical and neoclassical economic analysis of fiscal policy. Fiscal stimulus (deficit spending) could stimulate production. But to these schools, there was no reason to believe that this stimulation would outrun the side-effects that "crowd out" private investment: first, it would increase the demand for labor and raise wages, hurting profitability. Second, a government deficit increases the demand for money and encourages high interest rates, making it more expensive for business to finance fixed investment. Thus, efforts to stimulate the economy would be self-defeating. Worse, it would be shifting resources away from productive use by the private sector to wasteful use by the government.

The Keynesian response is that such fiscal policy is only appropriate when unemployment is persistently high, above what is now termed the "NAIRU". In that case, crowding out is minimal. Further, private investment can be "crowded in": fiscal stimulus raises the market for business output, raising cash flow and profitability, spurring business optimism. To Keynes, this accelerator effect meant that government and business could be complements rather than substitutes in this situation. Second, as the stimulus occurs, gross domestic product rises, raising the amount of saving, helping to finance the increase in fixed investment. Finally, government outlays need not always be wasteful: government investment in public goods that will not be provided by profit-seekers will encourage the private sector's growth. That is, government spending on such things as basic research, public health, education, and infrastructure could help the long-term growth of potential output.

Invoking public choice theory, classical and neoclassical economists doubt that the government will ever be this beneficial and suggest that its policies will typically be dominated by special interest groups, including the government bureaucracy. Thus, they use their political theory to reject Keynes' economic theory.

In Keynes' theory, there must be significant (slack in the labor market) before fiscal expansion is justified. Both conservative and some neoliberal economists question this assumption, unless labor unions or the government "meddle" in the free market, creating persistent supply-side or classical unemployment. Their solution is to increase labor-market flexibility, i.e., by cutting wages, busting unions, and deregulating business.

It is important to distinguish between mere deficit spending and Keynesianism. Governments had long used deficits to finance wars. But Keynesian policy is not merely spending. Rather, it is the proposition that sometimes the economy needs active fiscal policy. Further, Keynesianism recommends counter-cyclical policies, for example raising taxes when there is abundant demand-side growth to cool the economy and to prevent inflation, even if there is a budget surplus. Classical economics, on the other hand, argues that one should cut taxes when there are budget surpluses, to return money to private hands. Because deficits grow during recessions, classicals call for cuts in outlays -- or, less likely, tax hikes. On the other hand, Keynesianism encourages increased deficits during downturns. In the Keynesian view, the classical policy exacerbates the business cycle. In the classical view, of course, Keynesianism is topsy-turvy policy, almost literally fiscal madness.

The "Multiplier effect" and interest rates

Two aspects of Keynes's model had implications for policy:

First, there is the "Keynesian multiplier", first developed by Richard F. Kahn in 1931. The effect on demand of any exogenous increase in spending, such as an increase in government outlays is a multiple of that increase -- until potential is reached. Thus, a government could stimulate a great deal of new production with a modest outlay: if the government spends, the people who receive this money then spend most on consumption goods and save the rest. This extra spending allows businesses to hire more people and pay them, which in turn allows a further increase consumer spending. This process continues. At each step, the increase in spending is smaller than in the previous step, so that the multiplier process tapers off and allows the attainment of an equilibrium. This story is modified and moderated if we move beyond a "closed economy" and bring in the role of taxation: the rise in imports and tax payments at each step reduces the amount of induced consumer spending and the size of the multiplier effect.

Second, Keynes re-analyzed the effect of the interest rate on investment. In the classical model, the supply of funds (saving) determined the amount of fixed business investment. To Keynes, the amount of investment was determined independently by long-term profit expectations and, to a lesser extent, the interest rate. The latter opens the possibility of regulating the economy through money supply changes, via monetary policy. Under conditions such as the Great Depression, Keynes argued that this approach would be relatively ineffective compared to fiscal policy. But during more "normal" times, monetary expansion can stimulate the economy, mostly by encouraging construction of new housing.

Subsequent developments in Keynesian thought

After Keynes, Keynesian analysis was combined with classical economics to produce what is generally termed "the neoclassical synthesis" which dominates mainstream macroeconomic thought. Though it was widely held that there was no strong automatic tendency to full employment, many believed that if government policy were used to ensure it, the economy would behave as classical or neoclassical theory predicted.

In the post-WWII years, Keynes's policy ideas were widely accepted. For the first time, governments prepared good quality economic statistics on an ongoing basis and a theory that told them what to do. In this era of new liberalism and social democracy, most western capitalist countries enjoyed low, stable unemployment and modest inflation.

It was with John Hicks that Keynesian economics produced a clear model which policy-makers could use to attempt to understand and control economic activity. This model, the IS-LM model is nearly as influential as Keynes' original analysis in determining actual policy and economics education. It relates aggregate demand and employment to three exogenous quantities, i.e., the amount of money in circulation, the government budget, and the state of business expectations. This model was very popular with economists after World War II because it could be understood in terms of general equilibrium theory. This encouraged a much more static vision of macroeconomics than that described above.

The second main part of a Keynesian policy-maker's theoretical apparatus was the Phillips curve. This curve, which was more of an empirical observation than a theory, indicated that increased employment, and decreased unemployment, implied increased inflation. Keynes had only predicted that falling unemployment would cause a higher price, not a higher inflation rate. Thus, the economist could use the IS-LM model to predict, for example, that an increase in the money supply would raise output and employment -- and then use the Phillips curve to predict an increase in inflation.

The strength of Keynesianism's influence can be seen by the wave of conservative economists which began in the late 1940s with Milton Friedman. Instead of rejecting macro-measurements and macro-models of the economy, they embraced the techniques of treating the entire economy as having a supply and demand equilibrium. But unlike the Keynesians, they argued that the "crowding out" effects discussed above would hobble or deprive fiscal policy of its positive effect. Instead, the focus should be on monetary policy, which was largely ignored by early Keynesians. This monetarism had both an ideological appeal -- since monetary policy does not, at least on the surface, imply as much government intervention the economy. The monetarist critique pushed Keynesians toward a more balanced view of monetary policy, and inspired a wave of revisions to Keynesian theory.

Through the 1950s, moderate degrees of government demand leading industrial development, and use of fiscal and monetary counter-cyclical policies continued, and reached a peak in the "go go" 1960s, where it seemed to many Keynesians that prosperity was now permanent. However, with the oil shock of 1973, and the economic problems of the 1970s, modern liberal economics began to fall out of favor. During this time, many economies experienced high and rising unemployment, coupled with high and rising inflation, contradicting the Phillips curve's prediction. This stagflation meant that both expansionary (anti-recession) and contractionary (anti-inflation) policies had to be applied simultaneously, a clear impossibility. This dilemma led to the rise of ideas based upon more classical analysis, including monetarism, supply-side economics and new classical economics. This produced a "policy bind" and the collapse of the Keynesian consensus on the economy.

In the 1990s the "uncoupling" of money supply and inflation caused an increasing questioning of the original form of monetarism. The repeated failures of projections for economic recovery in Japan and the United States based on neo-classical synthesis models, as well as the failure of "big bang" marketization in the former Soviet Bloc, have encouraged the recent revival in Keynesian ideas, with particular emphasis on giving the Keynesian macroeconomic analysis theoretically sound foundations in microeconomics. These theories have been called new Keynesian economics. The heart of the new Keynesian view rests on microeconomic models that indicate that nominal wages and prices are "sticky," i.e., do not change easily or quicky with changes in supply and demand, so that quantity adjustment prevails. This is a practice which, according to economist Paul Krugman "never works in theory, but works beautifully in practice." This integration is further spurred by work of other economists which questions rational decision-making in a perfect information environment as a necessity for micro-economic theory. Imperfect decision making such as that investigated by Joseph Stiglitz underlines the importance of management of risk in the economy.

New classical economics relied on the theory of rational expectations to reject Keynesian economics. Most well-known is the critique by Robert Lucas, who argues that rational expectations will defeat any monetary or fiscal policy. But new Keynesians argue that this critique only works if the economy has a unique equilibrium at full employment. Price stickiness means that there are a variety of possible equilibria in the short run, so that rational expectations models do not produce any simple result.

In the end, many macroeconomists have returned to the IS-LM model and the Phillips Curve as a first approximation of how an economy works. New versions of the Phillips Curve, such as the "Triangle Model", allow for stagflation, since the curve can shift due to supply shocks or changes in built-in inflation. In the 1990s, the original ideas of "full employment" had been replaced by the NAIRU theory, sometimes called the "natural rate of unemployment." This theory pointed to the dangers of getting unemployment too low, because accelerating inflation can result. However, it is unclear exactly what the value of the NAIRU is -- or whether it really exists or not. While the Keynesian triumphalism of the 1960s is certainly not due for a revival, Keynesian ideas persist, often used to attain very conservative goals. Many observers find it hard to distinguish the new Keynesianism from old monetarism, except that the latter's emphasis on the money supply has been dropped or downgraded.

Of course, for a relatively open economy such as that of the United Kingdom and almost all other countries, this simple Keynesianism must be complemented by considerations of foreign exchange markets, foreign exchange rates, and the balance of payments. Also needed is an understanding of issues of long-term growth of potential. The open economy considerations which were the basis of the conservative or neo-liberal revival of policy, were then codified by Keynesian economists.

The journalist and economist Will Hutton regards Gordon Brown as being the first "real" Keynesian Chancellor of the Exchequer, although an argument could be made for Stafford Cripps and Roy Jenkins. U.S President Nixon once said that "we are all Keynesians now." But though Keynesian ideas have affected all of macroeconomics, it is hardly the only school of thought.

See also

phentermine allegra d acyclovir adipex aldara alesse ambien buspar buy phentermine carisoprodol celexa cheap viagra cholesterol cialis condylox cyclobenzaprine denavir diflucan effexor famvir ioricet flexeril flonase fluoxetine generic viagra imitrex levitra lexapro lipitor nexium ortho evra ortho tricyclen phentermine prevacid prilosec propecia prozac renova retin-a soma tramadol triphasil ultracet ultram altrex vaniqa viagra xenical yasmin zanaflex zithromax zoloft zovirax zyban

zyrtec![[Main Page]](../../../../upload/banner-blue-135.jpg)